Like many trustees at top-tier universities, Steve Stevanovich (A.B. ’85, M.B.A.’90) is a prolific donor to his alma mater, the University of Chicago.

After pledging $7 million in 2006 to endow the University’s Stevanovich Center for Financial Mathematics, Stevanovich was elected to UChicago’s Board of Trustees in 2009. In 2014, Stevanovich pledged another $10 million, which would later be used to endow the Stevanovich Institute on the Formation of Knowledge.

The pledges—at a time of University budget cuts for many academic programs—allowed the two academic centers to hire staff and pursue scholarly initiatives. The centers were also awarded their own campus buildings for offices, following expensive renovations.

But according to court documents made public earlier this year, it was the University—not Stevanovich—that picked up the tab. Stevanovich has not come close to fulfilling his pledges that were supposed to have financed the centers. Approximately $2.8 million of his earlier pledge remains unpaid, and he has not paid any of the $10 million that he pledged in 2014.

Stevanovich says that he is unable to fulfill the pledges due to the ongoing legal fallout resulting from his hedge funds’ ties to disgraced Minnesota businessman Thomas Petters, who was convicted in 2009 of running one of the largest Ponzi schemes in history.

Since 2010 the bankruptcy trustee responsible for unraveling the scheme has filed multiple ongoing lawsuits against Stevanovich, seeking to get back the hundreds of millions of dollars in profits that he and his hedge funds made between 2001 and 2006 from issuing high-interest loans that helped finance Petters’ fraud. Stevanovich had also been sued in 2013 for his funds’ ties to yet another Ponzi scheme.

Despite his legal troubles, Stevanovich promised a University gift officer in 2017 that UChicago would see his money soon. He said that his funds had ownership stakes in two very promising companies, collectively worth billions of dollars. The windfall from these assets, according to Stevanovich, would provide him with significant short-term liquidity and even open the possibility of a “nine-figure” donation in the future.

However, those valuations are now under legal scrutiny. The Securities and Exchange Commission (SEC) is investigating whether Stevanovich and his hedge funds committed securities fraud and profited by overvaluing at least one of these companies, Groen Brothers Aviation (GBA), to their investors, which include pension funds.

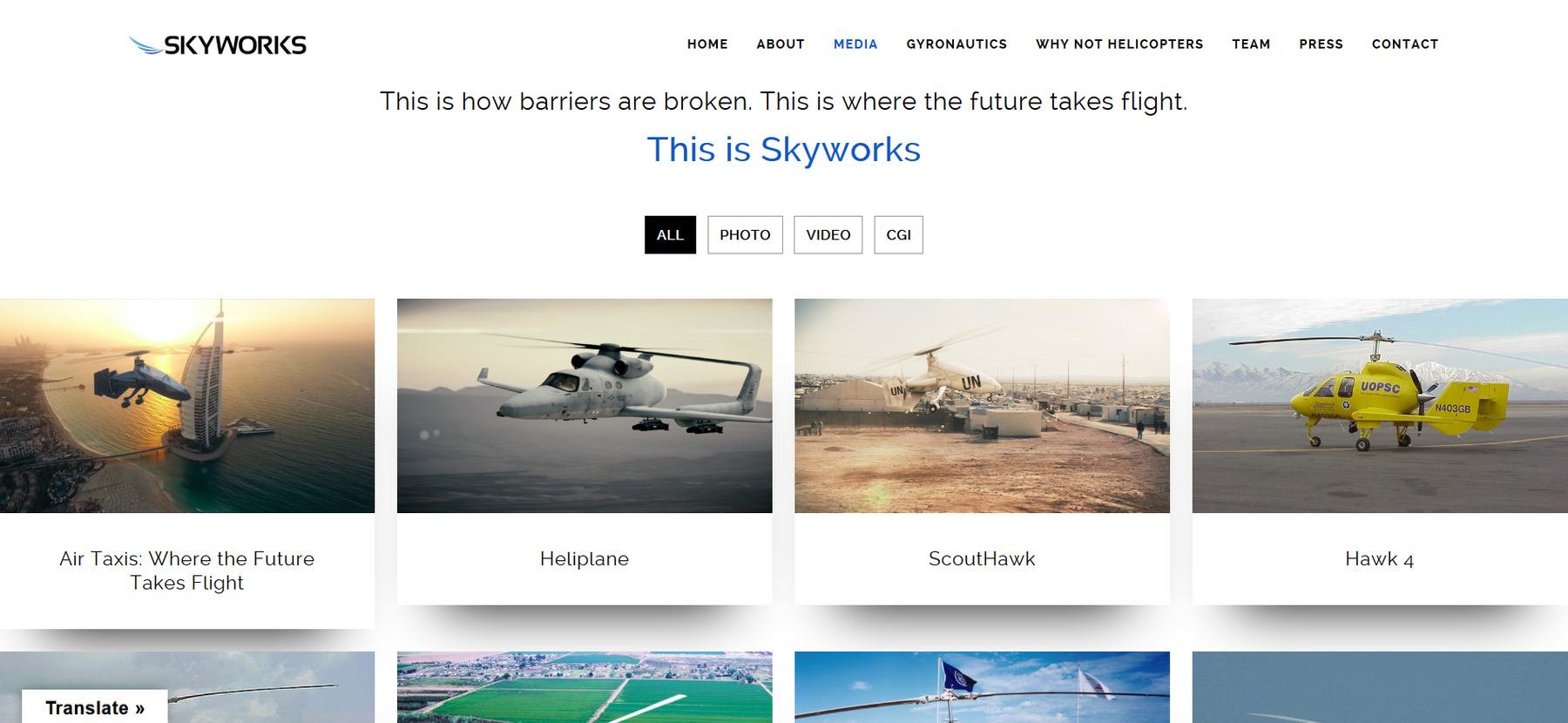

GBA, now known as Skyworks Global, has a website featuring computer-generated graphics of its aircraft flying over combat zones, and it lists the son of Jimmy Carter as one of its directors. But GBA currently has just one full-time employee. Meanwhile ex-employees have sued the company claiming that that they were owed hundreds of thousands of dollars in unpaid wages. One employee even claimed that he had to issue the company loans in the hundreds of thousands of dollars to keep the lights on.

Under Stevanovich’s control, GBA has pursued multiple joint ventures. One, based in the Chinese city of Wuhai, would have found the company simultaneously manufacturing gyroplanes and mining coal. But to date, none of these ventures have panned out.

Reached by e-mail, Stevanovich repeatedly denied that he was under SEC investigation, claiming its focus is another firm called West Mountain LLC. But while the investigation is indeed named after West Mountain, the SEC has explicitly stated that Stevanovich is under scrutiny.

“The SEC is investigating, among other things, whether Stevanovich and other persons affiliated with him made misrepresentations to investors regarding the value of hedge fund portfolios under their management,” one SEC filing said.

According to internal e-mails made public in court documents, the University did not anticipate Stevanovich’s failure to fulfill his pledges. It did not vet Stevanovich’s ability to pay, unlike most other large donors, because he was a trustee.

Stevanovich’s financial troubles have prompted messages from Board of Trustees Chair Joseph Neubauer to University President Robert J. Zimmer about whether the donations will actually materialize. But when asked whether it still had confidence in Stevanovich after being presented with this information, the University told The Maroon in a statement that it did.

“Mr. Stevanovich has been a valued Trustee of the University since 2009, during which time he has made a significant investment of time and personal resources. We are deeply grateful for his work in support of the University,” it read. “Because of a pending, complex legal proceeding in federal court, the University has agreed not to accept payments or new pledges from Mr. Stevanovich until the litigation is resolved. Similarly, Mr. Stevanovich has agreed to not make payments or pledges until the litigation is resolved.”

This isn’t the first time the University has faced difficulty in getting donors to fulfill their pledges. The Maroon reported earlier this year that the Pearson Family Foundation sued the University in February to recover $22.9 million it donated as part of its $100 million pledge to establish an academic center studying global conflicts. Alleging that the University failed to meet its end of the bargain, the Foundation expressed that it was also unwilling to pay the rest of the pledge.

Stevanovich’s Early Investments

After a career in investment management, Stevanovich in the late 1990s and early 2000s established a family of hedge funds that he directly controlled. The structure of these funds, which go by a variety of names including Westford, Epsilon, Capital Strategies, and SGS, is complex and not publicly known. Here, all of the funds under Stevanovich’s control shall be collectively referred to as the Westford Funds.

One of these funds’ major early investments was a $2.47 billion loan to the firms of Minnesota businessman Thomas Petters, composed of 344 transactions starting in 2001.

The interest rates on these loans were particularly high, allowing the funds to make an overall profit of around $280 million by the time they divested from Petters’ firms in 2007. Stevanovich, as the owner of several firms created to manage the funds, received a significant portion of the profits in the form of management fees.

The next year, Stevanovich pledged $7 million to the University to endow the Stevanovich Center for Financial Mathematics, which focuses on the quantitative study of markets. He would be appointed to the University’s Board of Trustees two years later.

But Westford and Stevanovich’s fortunes would soon change.

In 2008, federal investigators discovered that beginning in 1998, Petters had been running a $3.65 billion Ponzi Scheme, one of the largest in history. As part of the scheme, Petters convinced many investors that they were investing in legitimate businesses with great growth potential. In reality, he deposited their investments into a personal account and used new investors to pay older ones, taking a percentage of their assets for himself.

Westford’s seemingly unexplained decision to divest from Petters’ firms relatively shortly before the scheme’s collapse—which allowed it to profit off the fraud— raised questions about whether Stevanovich knew about the con. However, no court has ever found that Stevanovich was complicit.

In 2010, Douglas Kelley, the court-appointed trustee for the Petters estate, sued Stevanovich in the United States Bankruptcy Court of the District of Minnesota, hoping to reclaim for other investors either all the billions that Stevanovich’s funds received from Petters firms or just $323 million, representing the $280 million in profits along with their annual interest. These suits, called “clawbacks,” are common following the collapse of a Ponzi scheme; based on the theory that no one should profit from the fraud, they seek to take back money from those who benefited to distribute to the victims of a scheme.

Stevanovich strongly denied that he was aware that Petters was using the loans for illegal activity and played down Westford’s involvement in the scheme, noting that it had significant investments not related to Petters. One of these other investments was Groen Brothers Aviation (GBA), the company at the center of the SEC investigation.

GBA’s Beginnings

GBA was founded by David Groen and his late brother Jay Groen in 1986. The brothers envisioned developing and mass producing a gyroplane, a plane that could take off vertically like a helicopter but could also propel itself forward using gas turbine-powered propellers. The plane would supposedly be cheaper and safer to operate than a helicopter.

The company was promising. Its gyroplane prototype was named one of Time magazine’s inventions of the year in 2001 and GBA was awarded a $10 million Defense Advanced Research Projects Agency (DARPA) contract from the federal government to develop a heliplane in 2005.

According to court documents, Westford issued a series of loans to GBA starting in this period, which would eventually total at least $12 million.

However, the heliplane program was discontinued in 2008, eliminating a major source of funding for GBA. This funding shortfall, along with the severe recession that began that year, crippled the company’s finances. According to its SEC filing at the time, the value of GBA’s debt obligations grew dramatically as the company lacked resources to pay back loans.

By 2009, GBA owed $150 million to Westford, as a result of accumulated interest on the $12 million loan. Unable to make its loan payments, GBA signed a 2012 agreement with its creditors that eliminated its debts and in exchange gave them equity in a new company which took control of effectively all of its assets, such as its patents.

Westford—specifically an entity known as SGS Funds—became the largest shareholder of this new company with, according to later opponents in court, a 70 percent stake. This put GBA under Stevanovich’s control and completed what multiple documents describe as a “loan to own” strategy.

Under New Ownership

The new owners appeared to immediately breathe life into the struggling company. In July 2012, GBA announced that it had reached a very lucrative agreement with Zhongxin Group Ltd. Co., a technology investment company based in Hong Kong, to form a joint venture in China.

Under the terms of the deal, the joint venture would establish a large Aviation Industrial Park in Wuhai, a city with less than half a million people in the Inner Mongolia region of China. It would build a large number of gyroplanes for the park, based on GBA technology. With GBA still short on cash, Zhongxin agreed to provide much of the initial financing for the project.

Apart from building this park, the joint venture would simultaneously mine 20 million tons of coal allocated to it by the Wuhai municipal government —an amount worth over $1 billion according to JLL. Additional investment would also be matched with further coal allocations.

Support Our Staff On Financial Aid

Soon after the agreement was signed, Westford commissioned the Hong Kong office of Jones Lang LaSalle (JLL), an investment management company, to create a valuation of GBA. In a report issued in 2014, JLL valued GBA at $1.6 billion, based on the Wuhai deal and potential U.S. military uses of some of the company’s gyroplane models.

Westford also commissioned JLL to value its other major asset: ownership of Advanced Petroleum Technologies (APT). JLL valued the company, an energy technology firm, at $840 million.

GBA and APT comprised the vast majority of Westford’s assets in 2015, according to private documents obtained by the SEC. One of Westford’s main constituent funds, the Westford Master Fund, had 99% of its assets invested in the two companies. As a result, JLL’s reports dramatically increased the value of Westford’s assets to $1.3 billion, at least on paper.

However, those valuations may not have been accurate. JLL stressed in its 2014 valuation reports that it had heavily relied on information and assumptions provided by GBA and APT to assess the fair value of those companies, and that it had not independently verified their information.

“We would like to emphasize that this exercise [assessing fair value] is to a large extent based on information and assumptions provided by the Company and to stress that we have not performed legal authentication of the certificates provided nor verified the information and assumptions supplied to us,” JLL wrote in its GBA valuation report.

For instance, the report assumed that GBA would produce a considerable number of military gyroplanes, potentially to sell to the U.S. military. According to the SEC, however, none of the company’s military gyroplane product lines had been fully developed at the time of JLL’s report. There is also no indication that the product lines have been completed since then.

Furthermore, the Wuhai deal that justified a significant part of the JLL valuation ultimately fell through. Two years after signing the deal, GBA’s then-CEO, Jason Chen, withdrew the company from the Wuhai deal with board approval. He later said that he thought it could have exposed the firm to severe consequences.

“I continued to work on the Wuhai deal, and soon discovered it was fraught with illegitimacy and advised the deal be terminated,” he wrote in an affidavit. “With the support from Stevenovich [sic] and David Groen, I carefully terminated the deal in June 2014 to avoid potentially severe legal, political and business consequences.”

There was also no indication that the Chinese government had approved the joint venture and the allocation of tens of millions of tons of Wuhai coal to the company.

The Ministry of Commerce of the People’s Republic of China—the government authority that approves Sino-Foreign Cooperative Joint Ventures—did not respond to requests for comment.

Stevanovich maintains that the Wuhai deal would have been a boon for GBA, and he alleges that Chen withdrew the company from the joint venture for personal reasons. Reached by e-mail, he stood by the JLL report, saying its valuation, if anything, was too low.

He claimed that JLL’s report was audited by the Hong Kong branch of Crowe Global (formerly Crowe Horwath International), an accounting firm. He would not provide the audit to The Maroon.

Disgruntled Former Employees Demand Payment

On the ground, conditions at GBA following its acquisition were a far cry from what might be expected for a billion dollar company.

According to GBA’s Form 10-K—filed in 2012 around the time it was effectively acquired by Stevanovich and his Westford Funds—the company made $12,000 in revenues and ran an operating loss of $3.5 million that fiscal year. Court documents from all sides suggest that GBA did not receive significant investment from Westford nor any other party following its acquisition.

Expensive ongoing litigation due to Stevanovich’s links to the Petters scheme and an unexplained prior SEC investigation drained his personal liquidity and hampered efforts to attract investors to the Westford Funds, according to Stevanovich’s own admission and the court testimony of other parties.

Several former GBA employees say in court documents that the lack of investment had tangible effects.

Five former GBA employees, including Chen, and its former landlord filed an involuntary bankruptcy petition in 2017. They allege that their salaries were cut, that rent went unpaid, and that the company eventually missed paydays altogether. Chen even claims that he had loaned the company his own money to keep GBA afloat. By 2015, almost all of the full-time employees left the company, and much of GBA’s office equipment, including computers, was sold.

There is no indication that the company has done any significant hiring since then, and certainly not the hiring necessary to develop multiple gyroplane product lines. The former employees who filed the involuntary bankruptcy petition describe GBA now as having virtually no operations.

“Since reorganization by Stevanovich in 2012, the company has been a shell of a ‘technology company’ with no revenue and virtually no operations, or R&D,” the employees said in one motion.

The SEC supports this view, stating in a court brief in 2018 that GBA had only one full-time employee.

Lack of Oversight

Although not legally required, hedge funds often have their financial documents audited by a third party, so that investors can more easily judge the true value of investments like these. However, for at least one Westford Fund with a significant stake in GBA and APT, no current audited documents exist.

According to a court filing by the SEC, one of the main Westford Funds, called the Westford Master Fund, has not been audited since 2007, even though its governing documents require annual audits. And, in July 2013, the fund stopped using its fund administrator, which normally provides further accountability. Its purpose, according to an SEC filing, is to provide “independent, third-party verification of a fund’s asset values and trading positions.”

Shortly afterward in early 2014, Stevanovich increased the value of the Master Fund by over 250% to $741 million, on the strength of the JLL evaluations.

Stevanovich’s funds have faced multiple lawsuits related to their lack of transparency. In 2010, Seattle’s employee pension fund unsuccessfully sued one fund demanding audited financial statements and information on where its $20 million stake in the fund was invested.

Bridgestone Americas, which invested $75 million with Stevanovich, filed its own lawsuit in 2013. It said that it had not received audited financial documents since 2008, and demanded that an independent fiduciary be appointed to help run the fund that had its money. That suit was settled out of court.

The $10 Million Pledge

In early 2014, Stevanovich began discussions about another large gift to the University. But from the beginning, some administrators were concerned about his ongoing clawback lawsuits from the Petters scheme. Internal e-mails detailing these discussions were released in a later 2018 lawsuit.

“Steve [Stevanovich] reiterated that there is no possibility for clawback for a gift he might make from the Petters bankruptcy court,” Paul Seeley, one of the University’s gift officers, said in an April 2014 e-mail to colleagues. “My sense is that he’d like some reassurance the University has no such concern. Any gift he made — cash or securities, future gift or past giving to the center — would be vulnerable to such a clawback claim.”

Have a tip?

Fidelity Charitable, which the University asked to help facilitate the gift, was hesitant, citing concerns about the clawback lawsuits. This led Denise Chan Gans, another gift officer, to question the wisdom of accepting the gift without further consideration.

“The fact that Fidelity is declining a potential gift (at least initially) due to potential clawback concerns should raise red flags with us as well,” Gans said in an e-mail. “It would be my recommendation that…we have confirmation from the Board that they are comfortable accepting a gift from Steve Stevanovich at this point. This would protect us/the University later if any questions are raised and in a worst case scenario would show that a deliberate decision was made.”

Despite these concerns, the gift went ahead, and on April 30 Stevanovich pledged $10 million to the University. The pledge would later be designated for what became the Stevanovich Institute on the Formation of Knowledge, an interdisciplinary program focused on the study of knowledge-creation.

In a December 2014 e-mail, University gift officer Kenneth Manotti said that Stevanovich was planning to pay for the gift with private securities. Unlike publicly-traded assets, there usually isn’t an open market to buy and sell private securities, making it harder to fix their true value.

“He is going to give us securities - privately held which we will need to hold and sell at the appropriate time - which would be when he tells us,” Manotti said. “We expect to receive payment over the next 3-5 years but not clear how much each year.”

Manotti did not state which securities Stevanovich was planning to give, but at the time private stock in APT and GBA constituted the majority of Westford’s portfolio. Stevanovich would later assure another gift officer that the two companies’ increasing value would provide him with liquidity.

In October 2014, a preliminary settlement was reached between the Stevanovich funds and Kelley. The agreement called for the funds to return $322 million to the bankruptcy estate, representing their net profit from the Petters scheme along with annual interest.

As part of the settlement process, Kelley reviewed the financial records for many of the Westford funds. They apparently possessed no major assets aside from their stake in APT and Skyworks.

However, the settlement eventually fell apart. According to transcripts from a 2016 proceeding, Kelley withdrew from the process. But in 2017, Stevanovich appears to have told the University otherwise. According to a report filed by Seeley, Stevanovich claimed that he was the one to withdraw, after “the outcome of a similar case turned the suit in his favor.”

In an e-mail to The Maroon, Stevanovich reaffirmed the claim that he, not Kelley, broke off the settlement process.

“I can see how the other side might see it that way as our two sides could not come to terms,” Stevanovich said. “But we were unwilling to meet their demands at the time and walked away.”

Unpaid Pledges Raise Eyebrows

In 2016, as both the $10 million pledge and the $2.8 million from his previous pledge remained unpaid, Stevanovich’s delays caused questions among University administrators about the decision to accept the donation in the first place.

On December 10, Manotti emailed President Robert J. Zimmer after speaking with Joseph Neubauer, chair of the board of trustees. Stevanovich had told both the University and Neubauer that lack of liquidity was the main obstacle to fulfilling his pledges.

“According to Joe [Neubauer], Steve’s explanation is the same as with us,” Manotti said. “He expects to be liquid next year. I informed Joe that Steve has been saying this for the past 2 years.”

When Neubauer asked why the University did not research whether Stevanovich was able to fulfill his donations prior to accepting the 2014 gift, Manotti said that it was because Stevanovich is on the board of trustees. Neubauer then recommended that the University begin vetting trustees’ ability to pay.

“I told him that we do research [ability to pay] for many of our PG donors but we have not done this type of due diligence for our trustees (since I have been here),” Manotti said. “He told me that we should have a process for everyone including trustees and we should not trust what they say.”

Have something to buy or sell?

Stevanovich would later e-mail Neubauer on December 24 to discuss “unforeseen expenses for the [Stevanovich Institute] building renovation.” He said that liquidity still prevented him from paying his pledge, but offered to increase its size.

“I know that the repairs need cash, but I don’t know if a pledge increase can help in any way with internal allocations?”, Stevanovich said. “If that can help in any way, I’m happy to do so.”

In response, Neubauer suggested that $250,000 a year in cash would be more helpful to the Institute; Stevanovich declined, but said he would “try to work towards it in 2017.”

“As I suspected it may be a while until we see some real personal cash from Steve,” Neubauer wrote, forwarding the e-mail exchange to Zimmer. “However he is trying and we should stay with him next year.”

Legal Troubles Continue

In 2016, Petters trustee Doug Kelley filed yet another lawsuit, targeting a different Stevanovich-controlled fund and demanding nearly $400 million. In addition to Stevanovich, the suit named both GBA and a number of funds under Stevanovich’s control, alleging they were the recipients of Petters money transferred through Stevanovich funds. That lawsuit is ongoing.

In July 2017, at a lunch with Seeley, Stevanovich discussed the ongoing Petters case. In addition to claiming that he was the one who withdrew from the settlement process, Stevanovich said, according to Seeley, that once the process of discovery concluded for the Petters suits, he could resume paying back his pledges.

“Steve has avoided any giving to the University because he doesn’t want the Trustee [Kelley] to use it as a sign of profligacy or invite further harassment from the Trustee’s law firm,” Seeley reported according to an internal University report included as an exhibit by Kelley. “Apparently, the University received a subpoena from the Trustee asking for information about Steve’s giving. Discovery is supposed to conclude on January 1, ending the need to withhold all giving. Settlement is supposed to conclude by March 1.”

Stevanovich also touted the valuations of his two companies, claiming APT was worth $700 million and Skyworks (GBA) $1.7 billion and that both had the potential to be “multi-billion dollar companies.”

“Skyworks is the gyrocopter manufacturer formerly known as Groen,” Seeley reported. “Steve is exploiting the potential military applications and markets of the technology, hired a former general as CEO and recruited Senator Byron Dorgan, fellow member of the Argonne Board, to his advisory board.”

Finally, Stevanovich touted the possibility of a much larger gift to the University, though it would not be for the purpose of scholarships, according to Seeley.

“He wants to partner with the University [to] do something transformative in the same way as, but on a much larger scale than the Pearson brothers,” Seeley reported. “He doesn’t want to name or endow an existing structure, such as the College, and he doesn’t believe in scholarships, saying he paid his own way and others should as well. A nine-figure gift could be possible in the next five-ten years.”

Stevanovich, in an e-mail, said that he doesn’t focus his giving on scholarships but denied that he opposed them outright.

“I am not familiar with the document,” Stevanovich said. “If such a statement was made, however, it has misinterpreted my views. While scholarships are not one of my personal philanthropic priorities, I have never objected to any of the University’s scholarship initiatives either as a Trustee or in my personal capacity.”

Latest Developments

Kelley was informed in January 2018 of the existence of bank accounts in Hong Kong belonging to the Westford Funds, according to court documents. The accounts had never previously been disclosed in eight years of litigation, he said.

A few days later, Farrington Yates, a lawyer for Kelley, successfully requested a 90 day extension for the 2010 lawsuit’s discovery process. Stevanovich’s funds, according to a transcript of the hearing, tend to dispose of documents quickly, forcing Kelley to seek other ways to find the relevant information.

“Mr. Stevanovich has admitted that the document retention policy at these entities essentially allowed at the end of each year, at the very least, for documents to no longer be retained,” Yates said in a hearing. “That means we need to go out and try to fill holes through Mr. Stevanovich, which we tried to do, and through third parties.”

The involuntary bankruptcy complaint filed by Chen and others made a similar point, arguing that Stevanovich’s record keeping was consistently insufficient.

Furthermore, Yates specifically cited Stevanovich’s comments to Seeley as cause for concern.

“Stevanovich [made statements] to the representative at University of Chicago that makes it clear he was not taking any action with respect to that gift until the discovery cutoff passed,” Yates said. “He’s acutely aware of when discovery in this adversary proceeding is supposed to end; and that makes us very suspicious. I think the Court would agree that that might be reasonable under the circumstances.”

In April, Kelley filed yet another lawsuit against Stevanovich, this time also naming the University. The lawsuit sought to prevent any further payments to the University, arguing Stevanovich’s $10 million pledge was fraudulent since it was made when he was already facing a lawsuit from Kelley. Kelley included extensive exhibits, including internal University correspondence, which were publicly released.

On July 18, the University successfully moved to stay the case, arguing it could not go forward until a judgment was secured in the main lawsuit.

Earlier in January, the SEC first disclosed the existence of an investigation against Stevanovich. The SEC investigation concerns whether Stevanovich has misled investors in his funds by inflating their value, specifically mentioning APT and GBA.

“The Securities and Exchange Commission is investigating, among other things, a possible securities fraud involving material misrepresentations about the valuation of two companies,” the SEC said in a court filing.

The SEC also claims that Stevanovich is owed hundreds of millions of dollars in advisor fees from his funds. Since the fees depend on fund performance, inflating the funds’ value would increase them.

“Westford Management’s adviser fees are based on the fund’s performance, so higher fund values equate to higher fees,” the SEC said in another filing. As of September 2017, the funds managed by Stevanovich purportedly owed over $250 million in adviser fees.”

Stevanovich claims that he has not been paid these fees due to his funds’ lack of liquidity. However, the SEC wants to verify if he profited in some way off GBA and APT’s possible overvaluation.

Stevanovich has strenuously opposed the investigation. After a subpoena was filed against his accounting firm, Stevanovich instructed them not to comply; in response the SEC sued to enforce the subpoena, publicly disclosing the investigation for the first time.

Stevanovich sought to block the enforcement in court, arguing that his tax records are private and that documents already provided to the SEC should be enough. But the SEC defeated his motion, arguing that those documents could be fraudulent.

“The SEC’s experience is that those willing to violate the securities laws are always willing to cover up their misconduct,” the SEC said in a legal filing. “They do so in innumerable ways: phony invoices, phony account statements…fake check registers, fake calendar entries. They create the illusion of fake gold mines, fake factories, even fake airlines. And, they take care to keep the money that they steal.”

Kay Yang contributed reporting.

Euirim Choi (@euirim) is the Editor-in-Chief of The Maroon. He is a fourth-year in the College studying Computer Science and Economics.

Spencer Dembner (@spencerdembner) is a news editor. A second-year in the College, he is studying Mathematics and Philosophy.